Health insurance is one of those employees benefits most people appreciate having but hope they never need to use it.

Employees receive policy documents. HR explains the benefits. Insurance cards are issued. Emails are sent.

And when the actual time for hospital visits for a treatment, they do not know the answers related to their Employee Health Insurance policy. Instead, they ask:

“Is this treatment covered?”

“Do I need to stay in the hospital overnight?”

“Will a short hospital stay qualify for a claim?”

“Do I need approval before treatment?”

“Why did my colleague’s insurer accept the same treatment while mine did not?”

For years, many people have associated health insurance hospitalization claims with spending at least 24 hours in a hospital. No overnight stay often meant uncertainty about whether the medical expenses would qualify for coverage.

Healthcare has changed.

Procedures that once required patients to remain hospitalized overnight can now be completed within a few hours because of advances in medical technology.

Health insurance practices are changing, too.

Some health insurance policies may recognize eligible hospital stays lasting as little as two hours. This can make health insurance more relevant to modern medical care, but there is an important detail employees should understand.

A 2-hour hospitalization does not automatically mean your insurance claim will be approved.

Understanding medical insurance coverage is important for employees, employers, and HR teams because health benefits are most useful when people know how they work.

Why Are Health Insurance Rules Changing?

For years, health insurance claims were commonly associated with the traditional 24-hour hospitalization requirement.

Medical care has changed. Advances in surgical methods, diagnostic technology, treatment procedures, and recovery practices mean patients may no longer need to occupy a hospital bed overnight for many procedures.

A patient may:

- Enter the hospital in the morning.

- Complete the required medical treatment.

- Remain under observation.

- Receive discharge approval.

- Return home within hours.

The treatment can still be medically necessary even though the short stay hospitalization lasts only a few hours.

This creates an important question.

Should a patient lose access to medical insurance coverage simply because modern healthcare allows the treatment to be completed faster?

Changes in health insurance products and regulatory guidance help insurance practices respond to advances in healthcare.

But employees should understand one important point:

A shorter hospital stay does not remove the conditions written into the employee health insurance policy. Claim eligibility still depends on the policy of contract.

What Does 2-Hour Hospitalization Mean for Medical Insurance Coverage?

The term 2-hour hospitalization health insurance generally refers to health insurance coverage that may recognize eligible hospital admissions lasting for a shorter period than the traditional 24-hour hospitalization requirement.

For example, a patient may:

- Enter a hospital for a scheduled medical procedure.

- Complete the required treatment.

- Remain under medical observation.

- Receive post-treatment care.

- Get discharged after a few hours.

Depending on the insurance policy and treatment conditions, the hospitalization expenses may qualify for coverage.

This development is especially relevant because many modern medical procedures no longer require patients to occupy hospital beds overnight.

But the duration of the hospital stay is only one part of claim of eligibility.

The insurer may also review:

- Whether hospitalization was medically necessary

- Whether the treatment is covered under the policy

- Whether the hospital meets policy requirements

- Whether pre-authorization was obtained when required

- Whether waiting periods apply

- Whether the treatment falls under an exclusion

- Whether the required documents were submitted

Employees should understand that a shorter hospitalization period can make some treatments eligible for consideration, but it does not remove the other terms of the insurance policy.

To know more about this 2-hour hospitalization rule visit: Health insurance now covers hospital stays as short as 2 hours but read the fine print.

Why Isn't Every Short Hospital Stay Covered by Employee Health Insurance?

Imagine two employees working for different companies.

Both have employee health insurance.

Both undergo similar medical procedures.

Both remain in the hospital for four hours.

One claim is approved.

The other claim is denied.

Why?

Because insurance coverage depends on the individual policy.

One employee may have completed the required waiting period.

The other may still be within it.

One insurance policy may recognize the procedure under eligible hospitalization.

Another may classify the treatment differently.

One employee may have received pre-authorization.

Another may not have followed the required process.

One hospital may be part of the insurer's cashless network.

Another hospital may require reimbursement or may not meet the policy conditions.

This is why employees should never assume that another person's claim experience determines their own medical insurance coverage.

The policy document remains the most reliable starting point.

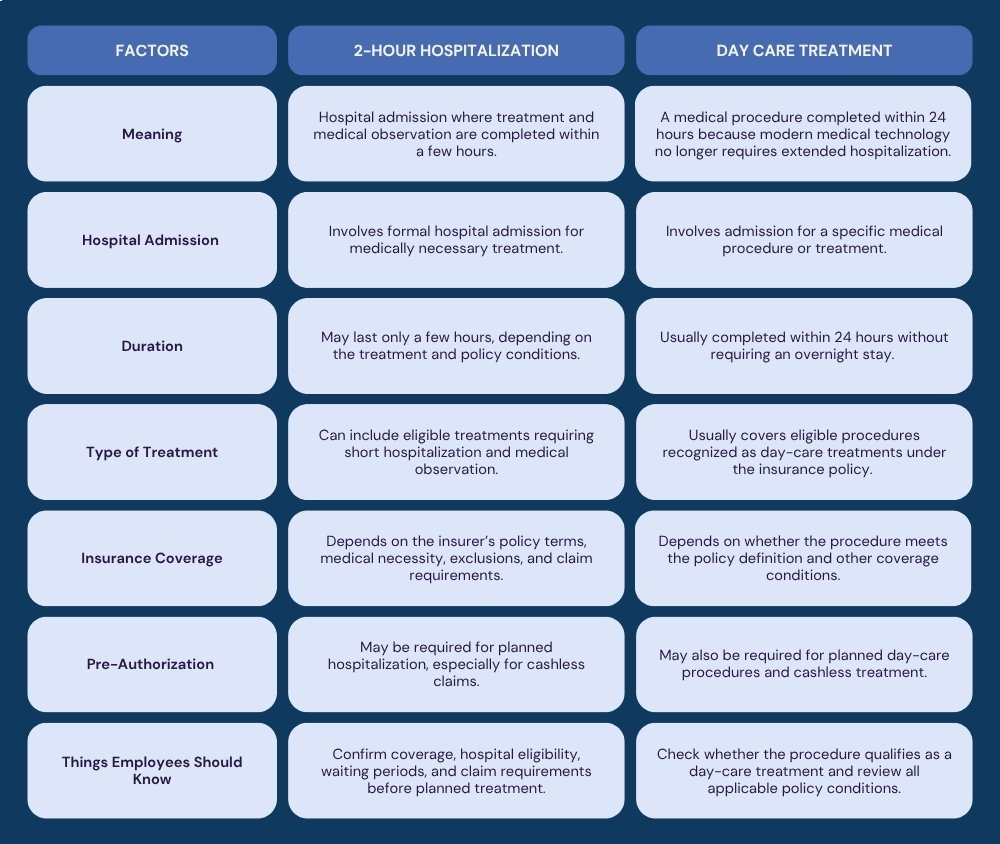

Is 2 Hour Hospitalization the Same as Day-Care Treatment?

Not always. Although both may involve treatment without an overnight hospital stay, the way they are defined and assessed for medical insurance coverage can differ.

What Should Employees Check Before Planned Hospitalization?

Nobody wants to search through insurance documents while preparing for medical treatment. Employees should understand the basic requirements before a planned health insurance hospitalization.

1. Confirm Whether the Treatment Is Covered

Employees should check whether the planned procedure or treatment qualifies under their insurance policy. If the policy's wording is unclear, they can contact the insurer, third-party administrator, hospital insurance desk, or HR team.

2. Check Whether Pre-Authorization Is Required

Many planned cashless treatments require prior approval. Employees should confirm when the request must be submitted and which medical documents are required.

3. Check the Hospital Network

Employees should confirm whether the hospital is part of the insurer's eligible cashless network. Treatment at a non-network hospital may require the employee to pay the expenses and later submit a reimbursement claim.

4. Review Waiting Periods

Certain medical conditions and procedures may have waiting periods. A medically necessary treatment may still not qualify for immediate coverage if the applicable waiting period has not been completed.

5. Understand Exclusions, Co-Payments, and Limits

Insurance policies may exclude certain treatments or place limits on specific medical expenses. Employees should understand which costs may remain in their responsibility.

6. Keep the Required Documents

Employees may need medical reports, prescriptions, hospital bills, diagnostic reports, payment receipts, authorization documents, discharge summaries, and claim forms. Complete documentation can reduce unnecessary delays during claim processing.

What Does IRDAI Say About 2-Hour Hospitalization?

The Insurance Regulatory and Development Authority of India regulates the insurance sector and issues rules, circulars, and consumer guidance related to health insurance in India.

IRDAI’s health insurance framework recognizes that advances in medical treatment have reduced the need for traditional 24-hour hospitalization in some cases. Policyholders should refer to their insurance contract, policy definitions, exclusions, waiting periods, and claim procedures when determining whether a short hospital stay or day-care procedure is eligible for coverage.

Employees should also confirm coverage with their insurer or third-party administrator before planned treatment whenever possible.

For official health insurance rules and consumer information, visit the IRDAI official website.

How HR Management Software Can Make Employee Benefits Information Easier to Access

Health insurance information is often scattered.

One document is in an email.

Another is in a shared drive.

The insurance card is stored somewhere else.

The claim process was explained during onboarding six months ago.

The latest policy update was shared in a chat group.

When an employee needs medical treatment, this scattered information becomes a problem.

HR software can help businesses organize benefit information in a central place.

Employees can use employee self-service portal access to find policy documents, benefit guides, announcements, insurance contacts, and other workplace resources.

HR teams can publish benefit updates without sending the same document repeatedly.

Policy acknowledgement of records can help organizations confirm that important benefit information has been shared.

Employee records can help HR maintain benefit eligibility and dependent information.

A company intranet can provide a clear space for FAQs, announcements, benefit guides, and employee resources.

HR software cannot guarantee that an insurance claim will be approved.

It can help employees find the information they need before they submit one.

How HR Teams Can Help Employees Understand Health Insurance

1. Explain Employee Benefits Clearly During Onboarding

Health insurance should not be explained through a policy PDF attached to a welcome email and never discussed again. During employee onboarding, HR can explain the basics:

- Who is covered

- How employees access insurance cards

- Where policy documents are stored

- How to check network hospitals

- Whom to contact during hospitalization

- How to start a claim

- Where to ask questions

A simple introduction can prevent confusion later.

2. Create a Health Insurance Help Page

Employees often ask the same questions. Instead of answering each query individually, HR can create a central benefits page containing:

- Policy documents

- Claim process guides

- Insurance contacts

- Network hospital links

- Frequently asked questions

- Emergency procedures

- Benefit announcements

Employees get faster answers, and HR receives fewer repeated questions.

3. Communicate About Policy Changes

Insurance benefits may change during renewals.

- Coverage conditions may change.

- Network hospitals may change.

- Claim processes may change.

Employees should know when important updates happen.

4. Keep Benefit Documents Current

Outdated policy documents can create serious confusion.HR teams should regularly review employee benefit information and remove or archive old documents.

5. Encourage Employees to Ask Questions Early

The hospital waiting room is not the ideal place to discover that pre-authorization was required. HR teams can encourage employees to review benefit information and ask questions before planned treatments.

Your Employees Have Health Insurance. Can They Find the Right Information When They Need It?

Employee health insurance benefits should not become a folder employees search for only when someone is admitted to a hospital.

Providing employee health insurance is an important benefit for employees. Making the information easy to understand and access is just as important.

Employees should not have to search through old emails, message threads, and shared folders to find policy documents, insurance contacts, claim guides, or important benefit updates.

With HR HUB, businesses can keep employee information, benefit documents, policy updates, acknowledgements, announcements, and self-service resources connected to one HR platform.

Employees get a clearer place to find important information. HR teams can communicate employee benefit updates more consistently and spend less time answering the same questions repeatedly.

Frequently Asked Questions

What is 2-hour hospitalization in health insurance?

A 2-hour hospitalization generally refers to a short hospital admission where medically necessary treatment and observation are completed within a few hours. Coverage depends on the employee health insurance policy, treatment, exclusions, and claim conditions.

Can HR confirm whether an employee's insurance claim will be approved?

No. HR can help employees access policy information, claim procedures, and insurance contacts, but the insurer assesses the claim according to the policy terms.

How can HR management software help with employee health insurance?

HR management software can help businesses organize insurance documents, policy updates, employee benefit information, acknowledgements, and self-service resources so employees can find important information more easily.