For years, PF-related work has been one of those tasks that quietly sits on every HR and payroll team's desk.

An employee joins the company. HR collects documents. Payroll calculates deductions. UAN details are checked. KYC information needs to match. Bank details must be corrected. Then, when an employee exits or applies for withdrawal, the same information becomes important again.

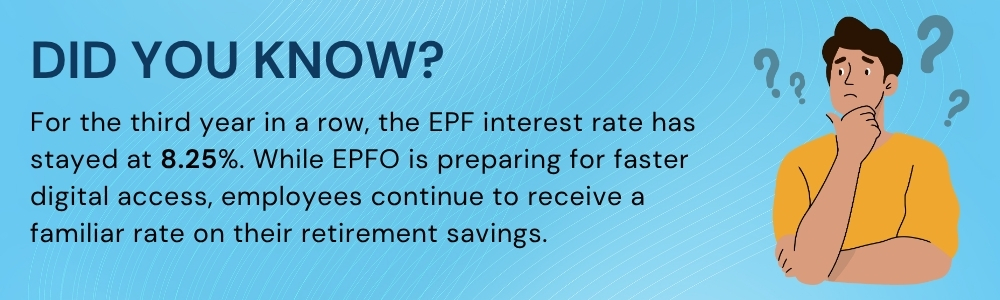

Now, with EPFO 3.0 New Rules, India is moving toward a more digital and faster way of managing provident fund services. In the recent announcement, EPF interest rate 2025-26 is set of 8.25%.

One of the most discussed updates is the possibility of UPI PF withdrawal, where eligible employees may be able to access their provident fund more quickly through digital channels. Earlier, there was also discussion around ATM-based PF access, and this takes that idea further by focusing on faster, simpler, EPFO digital services.

For employees, this sounds like convenience.

For employers, HR teams, and payroll teams, it is a reminder that clean employee data is no longer optional.

But here is the real question for businesses.

If employees can access PF withdrawal process faster, is your HR team and payroll management ready to support that speed?

Because even the fastest digital system can slow down when employee records are incorrect.

What is EPFO?

EPFO stands for Employees' Provident Fund Organization.

It manages provident fund benefits for eligible employees in India. Every month, both the employee and employer contribute toward the employee's EPF account. Over time, this becomes an important retirement and financial safety fund.

For employees, EPFO is linked to long-term savings.

For employers, EPF is linked to payroll compliance. That means HR and payroll teams must carefully manage:

- Employee details

- Salary information

- PF contributions

- UAN records

- KYC details

- Joining dates

- Exit dates

- Statutory records

If any of this information is wrong, employees may face problems during PF transfer, withdrawal, or claim settlement.

What is EPFO 3.0?

EPFO 3.0 refers to the next phase of digital changes expected in EPFO services. The focus is simple: make provident fund services faster, easier, and more accessible for employees.

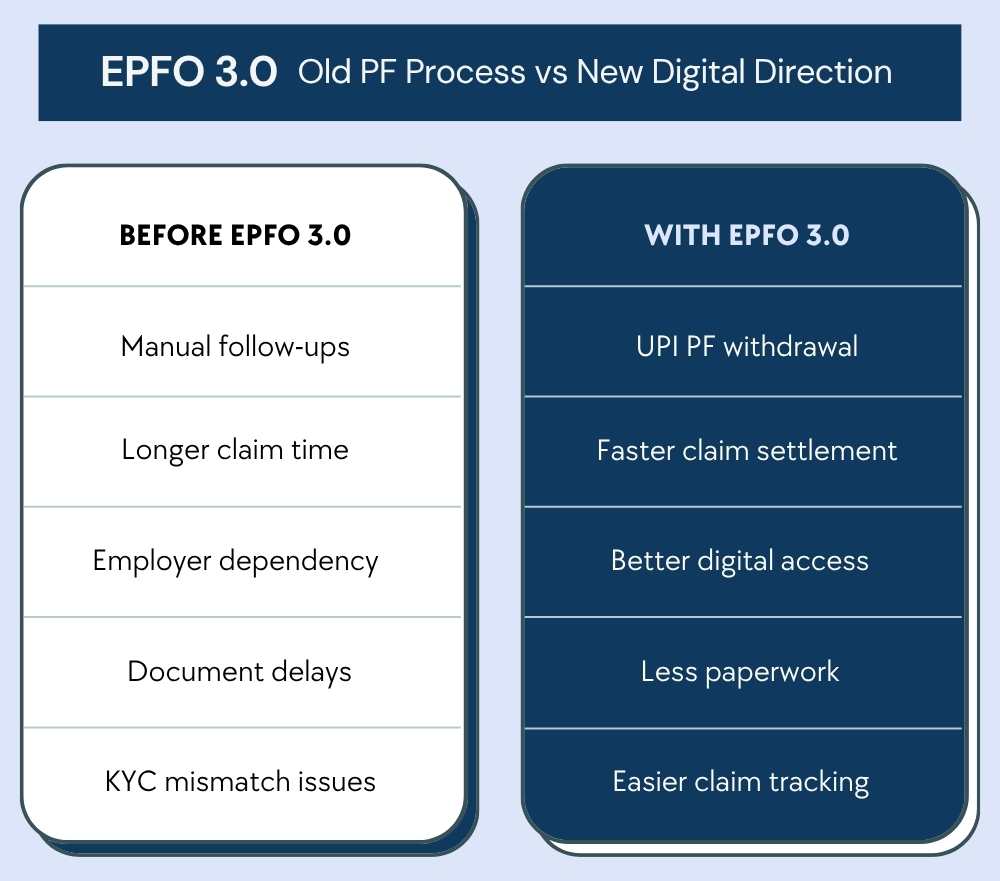

The goal of EPFO 3.0 is to reduce the old pain points that employees and HR teams have faced for years.

These include:

- Long PF withdrawal processing time

- Too much paperwork

- Repeated employer dependency

- Delays due to incorrect employee details

- KYC mismatch issues

- Confusing claim categories

- Slow claim tracking

- Manual follow-ups

The EPF interest rate 2025-26 has been kept at 8.25%. For employees, this directly affects their long-term savings.

For HR and payroll teams, it also increases the need for clean payroll records because EPF contributions are linked to salary details, employee information, joining dates, exits, and statutory deductions.

If payroll data is wrong, it can create issues such as:

- Incorrect PF contribution

- Employee complaints

- Mismatch in statutory records

- Delayed claim processing

- Compliance gaps during audits

This is why EPFO 3.0 is not only an employee update. It is also an HR and payroll operations update.

What Was the Problem Before EPFO 3.0 New Rules?

Let us look at this from a real HR team perspective. An employee wants to withdraw PF. The employee asks HR:

- "Is my UAN updated?"

- "Is my Aadhaar linked?"

- "Is my bank account correct?"

- "Why is my claim pending?"

- "Do I need employer approval?"

- "Why is my previous employer not approving the request?"

- "Where can I check my claim status?"

Now multiply this by 50, 500, or 5,000 employees.

That is when PF withdrawal process becomes more than a government process. It becomes a daily HR support challenge. Before digital upgrades like EPFO 3.0, many companies faced common problems such as:

- Employee data stored in Excel sheets

- Missing KYC documents

- Incorrect bank account details

- Delayed exit updates

- Salary mismatch in payroll records

- Manual statutory calculations

- Lack of document tracking

- Repeated employee follow-ups

- Poor visibility for HR and employees

The problem was not only with the PF withdrawal process. The bigger issue was scattered employee data.

If HR data is not clean inside the company, employees may face delays outside the company.

That is why EPFO 3.0 is not just an employee update. It is also a wake-up call for HR and employers.

EPFO 3.0 New Rules: What Changes It Will Bring?

The exact rollout and final process may depend on official EPFO notifications, but based on current updates, EPFO 3.0 is expected to bring major digital improvements. Here are the key changes you should know.

1. UPI PF Withdrawal

The biggest talking point is UPI PF withdrawal. It may allow eligible employees to withdraw PF through UPI-linked digital channels. If rolled out smoothly, this can make PF access faster and easier.

For employees, it may reduce waiting time. For HR teams, it may reduce basic follow-up queries.

But it also means employee details must be correct before the withdrawal request is made.

2. ATM-Based PF Access

ATM-based PF withdrawal has also been discussed as part of faster PF access. The idea is to give employees easier access to eligible PF amounts without going through a long manual process. This can be useful during emergencies, especially when employees need quick access to funds.

3. Faster Claim Settlement

EPFO 3.0 is expected to support faster claim settlement through digital verification and reduced manual intervention. This can help employees get quicker access to funds for approved reasons.

4. Better EPFO Digital Services

The larger goal is to improve EPFO digital services so employees can complete more tasks online. This may include better claim tracking, faster verification, and easier access to account-related information.

5. Reduced Employer Dependency

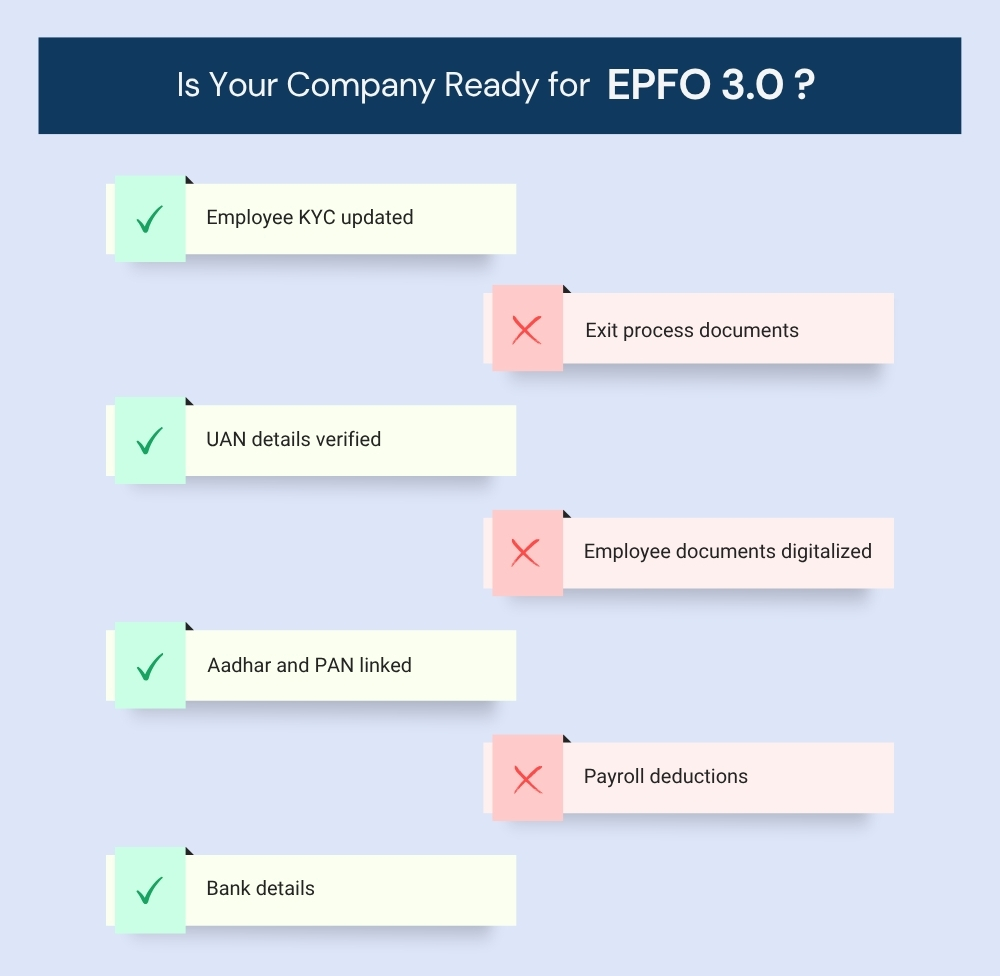

In many cases, employees depend on current or previous employers for PF-related actions. EPFO may reduce some of this dependency through digital KYC and verified records. But employers still have one important responsibility.

They must keep employee information correct while the employee is working with them.

Why Should Companies Pay Attention to New Rules for PF Withdrawal Process?

Many companies may think:

"EPFO 3.0 is for employees, not for us."

That is not fully correct.

EPFO may manage the PF withdrawal process, but employers are responsible for maintaining the employee data that supports PF compliance.

If company records are wrong, employees may still face delays.

Where HR Management Software Fits In Payroll Process?

HR Management Software helps companies manage employee data, payroll records, documents, and statutory information in a more organized way.

For EPFO 3.0 New Rules, this becomes even more important.

A good HR Management Software will prepare you for EPFO 3.0:

- Store employee records centrally

- Track statutory details

- Maintain payroll history

- Keep employee documents safe

- Support audits

- Reduce manual errors

- Improve employee self-service

EPFO digital services may improve the external PF service experience, but companies still need internal readiness.

In simple words:

EPFO can make the employee side faster.

HR Management Software helps make the employer side cleaner.

Both are needed.

Build an HR Operations That's Ready for Tomorrow

EPFO 3.0 is more than a policy update. It's a sign that HR, payroll, and compliance are becoming increasingly digital, connected, and employee centric. Businesses that continue to rely on manual processes will find it harder to keep pace with changing regulations and growing employee expectations.

HR HUB helps organizations simplify every aspect of workforce management, from employee onboarding and payroll processing to attendance, leave, document management, and statutory compliance. With accurate employee records, automated workflows, and centralized data, your HR team can spend less time managing paperwork and more time driving business growth.

Frequently Asked Questions

1. What is EPFO 3.0?

EPFO 3.0 is the next phase of digital updates expected from the Employees' Provident Fund Organization. It focuses on faster PF services, better digital access, and simpler claim-related processes.

2. What is the EPF interest rate 2025-26?

The EPF interest rate 2025-26 is reported as 8.25%, continuing the same rate for the third consecutive year.

3. When will EPFO 3.0 start?

EPFO 3.0 has been announced, but its features are expected to be introduced in phases. Employees and employers should follow official EPFO notifications for confirmed rollout dates and feature availability.

4. Can I withdraw PF using UPI?

UPI PF withdrawal is one of the key features proposed under EPFO 3.0. Once officially rolled out, eligible members may be able to withdraw their provident fund through UPI-enabled digital channels, making the process quicker and more convenient.

5. Is employer approval required?

EPFO 3.0 aims to reduce employer dependency for certain PF-related services through digital verification and Aadhaar-based authentication. However, some requests may still require employer involvement depending on the type of claim and the employee's records.

6. Does EPFO 3.0 affect pension benefits?

No, EPFO 3.0 primarily focuses on improving digital access to EPF services, such as claim processing and withdrawals. It does not change the existing Employees' Pension Scheme (EPS) benefits or pension eligibility rules.

7. Will my UAN change?

No. Your Universal Account Number (UAN) will remain the same. EPFO 3.0 focuses on improving digital services and claim processing, not changing existing UANs or member account details.