Your salary just changed.

India's 65-year-old tax law

And yes, your ATM charges just changed.

That changed, too.

April 1, 2026, is not just the start of a new financial year; it's the start of a whole new rulebook. India has implemented its most sweeping financial and regulatory overhaul in over six decades.

From the replacement of the Income Tax Act, 1961, with the new Income Tax Act, 2025, to revised banking charges, fuel pricing, and railway refund rules, the changes span every dimension of personal and corporate finance.

The New Income Tax Act, 2025

The Income Tax Act, 2025, replaces the Income Tax Act, 1961, in its entirety, effective from 1st April 2026. The primary objective is to simplify taxation, reduce legal ambiguity, and make compliance more accessible for everyday taxpayers. The new law uses plain language, removes redundant provisions, and restructures the entire framework in a logical sequence.

For most individual taxpayers, actual tax liability remains unchanged; rates, deductions, and exemptions are preserved. The change is largely structural and procedural.

New Income Tax Rules, 2026

The Central Board of Direct Taxes (CBDT) has notified the Income Tax Rules, 2026, which replace the decades-old Income Tax Rules, 1962. These revised rules align with the new Act and introduce updated deduction limits, revised PAN requirements, and new reporting forms.

Below are the key monetary limits revised under the new rules:

Impact for salaried employees: The enhanced meal card, education allowance, and hostel allowance limits translate to meaningful annual tax savings. HR teams should update payroll configurations immediately.

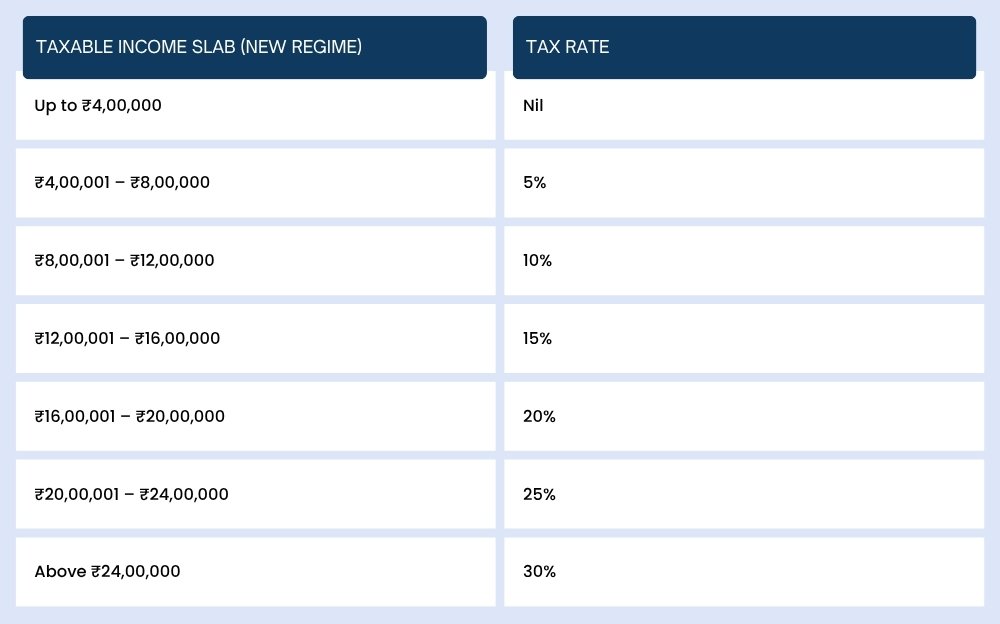

Income Tax Slabs for FY 2026-27; No Change

Tax slabs remain unchanged for FY 2026-27 under both regimes. The new tax regime continues as the default option.

Under the old tax regime, taxable income up to ₹5 lakh remains tax-free. Both regimes continue to coexist, giving taxpayers the flexibility to choose the more beneficial option.

Introduction of the 'Tax Year' Concept

The terms 'Financial Year' and 'Assessment Year', long a source of confusion for millions of taxpayers, are replaced by a single unified term: Tax Year. Under the old system, income earned in the previous year, 2025-26, was assessed in the Assessment Year 2026-27, creating a two-year overlap in terminology.

From April 1, 2026, the year in which income is earned and the year in which the return is filed are both referred to as the Tax Year. Tax Year 2026-27 spans from April 1, 2026, to March 31, 2027.

Note: Income earned in FY 2025-26 continues to be governed by the Income Tax Act, 1961. Only returns filed in 2027 for Tax Year 2026-27 fall under the new Act.

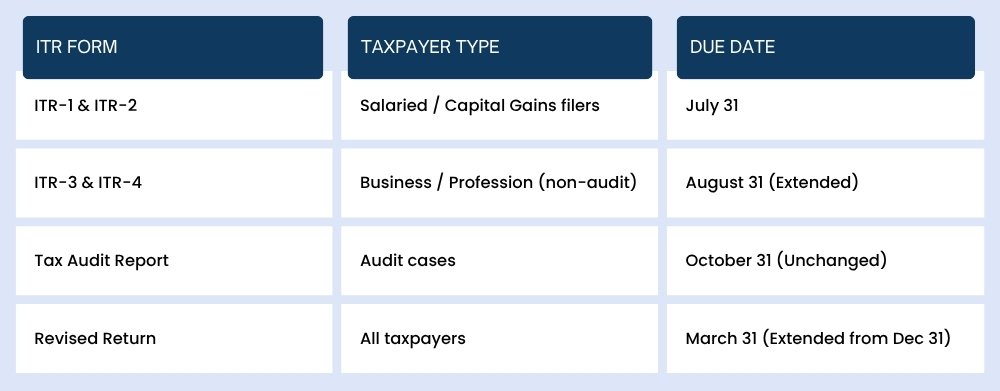

ITR Filing Due Date Changes

The ITR filing deadline for non-audit taxpayers filing ITR-3 and ITR-4 has been extended to August 31. This change applies from FY 2025-26 (AY 2026-27) itself. The due dates for other forms remain as follows:

Additionally, the due date for filing a revised return has been extended to 12 months from the end of the relevant tax year (i.e., March 31). Earlier, it was 9 months (as of December 31). However, taxpayers filing revised returns after December 31 will be required to pay an additional fee.

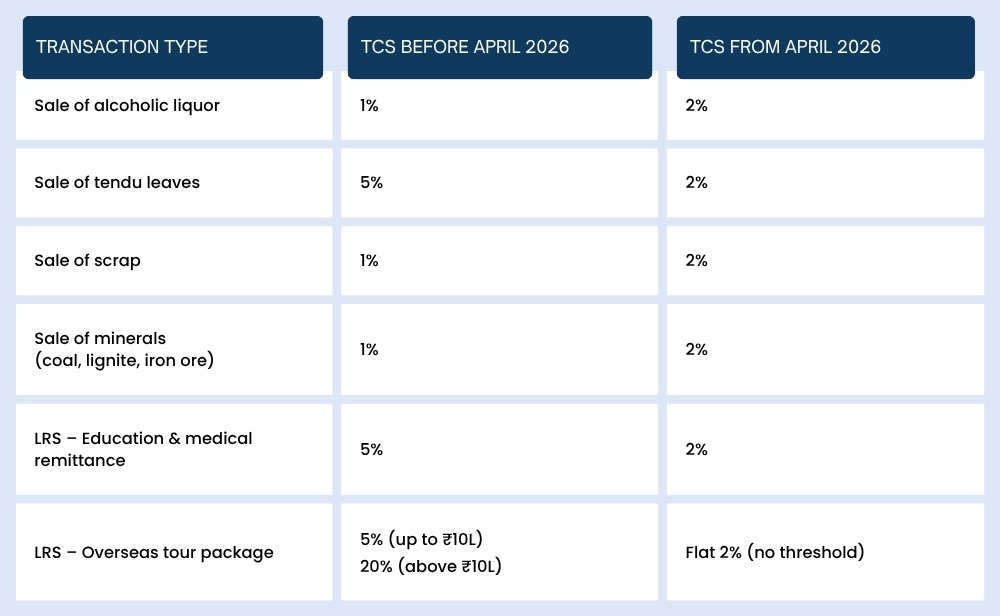

Tax Collected at Source (TCS); Revised Rates

TCS rates have been rationalized from April 2026 to ease compliance, reduce refund delays, and simplify the structure. Key changes are summarised below:

The simplification of TCS on overseas tour packages, from a dual-rate structure to a single flat rate of 2, is particularly welcome for individuals and travel businesses.

Extended Due Date for Revised Returns

Taxpayers who need to correct errors or omissions in their original return now have until March 31 (instead of December 31) to file a revised return. This gives an additional 3 months. An additional fee applies for revised returns filed after December 31.

The due date for belated returns (for those who missed the original deadline) remains unchanged.

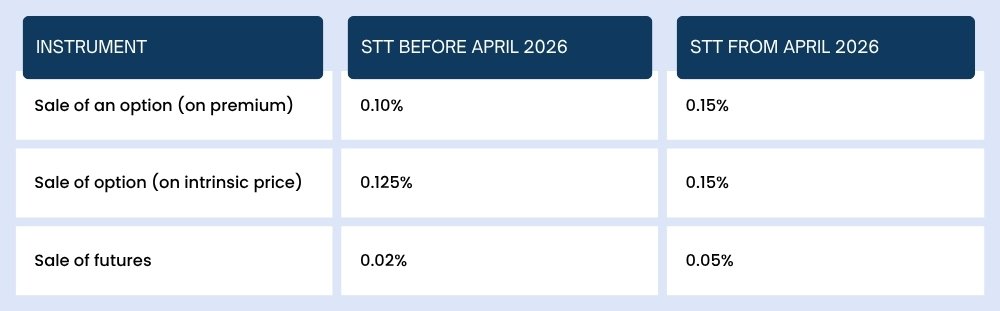

Securities Transaction Tax (STT); Increased for F&O Traders

STT rates on derivatives have been hiked from April 2026, resulting in higher transaction costs for futures and options (F&O) traders. This is one of the changes that directly increases the cost of trading for active market participants.

F&O traders should factor in the higher STT when calculating their cost-to-trade. The increased rate on futures is particularly significant, rising from 0.02% to 0.05%, a 2.5x jump.

Buyback Taxation: Shifted to Capital Gains

Before April 2026, amounts received from a company's share buyback were treated as deemed dividends and taxed at the applicable slab rate. From April 1, 2026, buyback proceeds will be taxed as capital gains in the hands of the shareholder.

The effective tax rate on buyback proceeds will be 30% for individual promoters and 22% for a company selling entity. Investors should recalibrate their buyback strategies in light of this change.

TDS on Property Purchased from NRIs; Simplified

Buyers purchasing immovable property from a Non-Resident Indian (NRI) no longer need to obtain a TAN (Tax Deduction and Collection Account Number) registration to comply with TDS requirements under Section 194IA. A simple PAN-based challan is now sufficient.

This is a meaningful simplification of compliance, particularly for individual property buyers who were previously deterred by the TAN registration process.

Interest Deduction on Dividend Income; Removed

Until FY 2025-26, taxpayers were permitted to deduct interest expenditure (up to 20% of dividend income) when computing their taxable dividend income. This allowed investors who borrowed funds to purchase dividend-yielding shares to reduce their tax liability.

From April 1, 2026, this deduction has been withdrawn for both dividend income and income from mutual fund units. Investors with leveraged portfolios should reassess their structures accordingly.

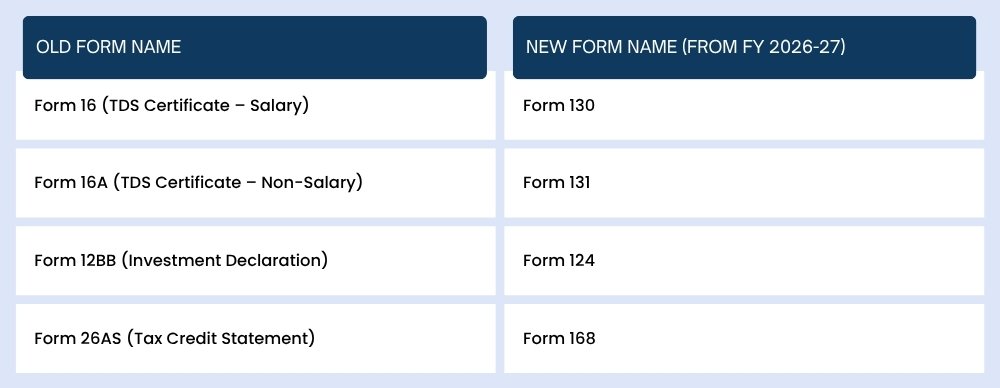

New Income Tax Forms; Renumbered

Under the Income Tax Rules, 2026, all existing income tax forms have been renumbered. The content and purpose of these forms remain the same; only the form numbers change. Taxpayers and CAs should familiarise themselves with the new numbering before the ITR filing season begins.

HR and payroll teams: Update your HRMS and payroll software to generate the newly numbered forms. Employees will now receive Form 130 instead of Form 16 for their salary TDS certificate.

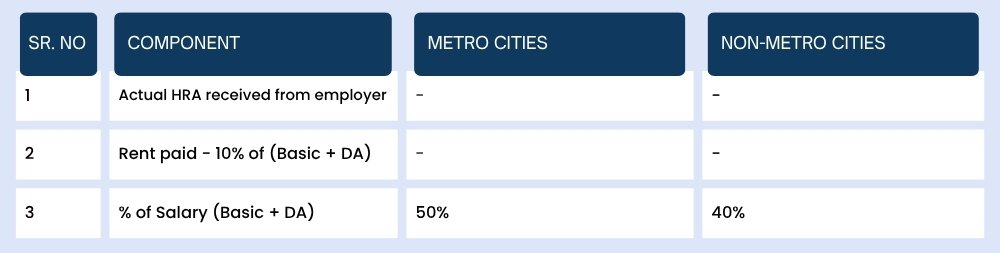

HRA Exemption; More Cities Added

The 50% HRA exemption (available for employees living in metro cities) has been extended to include Bengaluru, Pune, Hyderabad, and Ahmedabad. Previously, only Delhi, Mumbai, Chennai, and Kolkata qualified for the 50% rate.

From April 1, 2026, employees residing in any of the following 8 cities are eligible for 50% HRA exemption:

- Delhi

- Mumbai

- Chennai

- Kolkata

- Bengaluru

- Pune

- Hyderabad

- Ahmedabad

Additionally, taxpayers claiming the HRA exemption will now be required to disclose their relationship with the landlord. This is to curb fraudulent HRA claims made through relatives.

The 8 metro cities now eligible for 50% HRA exemption: Delhi, Mumbai, Chennai, Kolkata, Bengaluru, Pune, Hyderabad, Ahmedabad

All remaining cities: 40% cap (unchanged)

How is the HRA exemption calculated?

Only the metro city list has expanded. The formula: least of actual HRA received, 50% / 40% of salary, or rent paid minus 10% of salary, remains unchanged.

The exempt amount is the lowest of these three:

New Income Tax Utility Tool

The Income Tax Department has released an official online utility tool to help taxpayers, CAs, and tax professionals compare section numbers between the Income Tax Act, 1961, and the new Income Tax Act, 2025. This is particularly useful for those who need to cross-reference old and new section numbers in forms, software, and legal documents.

The tool is available on the official Income Tax India portal at incometaxindia.gov.in

Beyond Income Tax: Other Major Changes from 1st April 2026

While the income tax overhaul grabs the headlines, April 1, 2026 also brings significant changes to banking, fuel pricing, travel, digital payments, and identity rules. Here is a concise overview of everything else that changes this financial year.

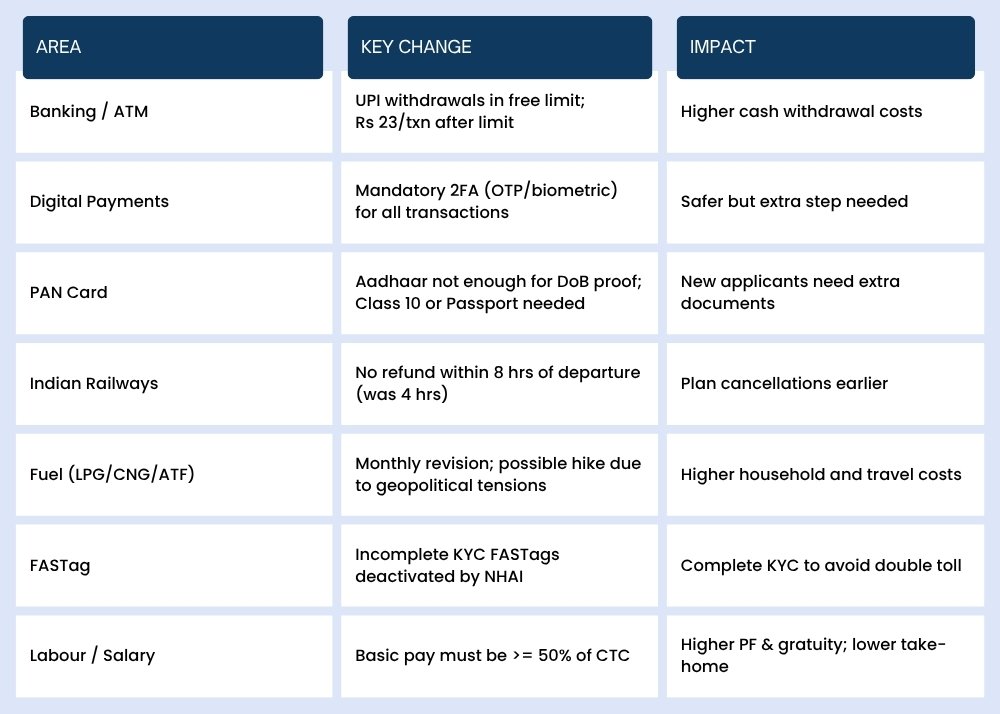

BANKING Banking & ATM Charges

- UPI-based ATM withdrawals are now counted within your monthly free transaction limit (HDFC Bank).

- After the free limit is exhausted, a charge of Rs 23 per transaction (plus applicable taxes) will apply.

- PNB has reduced daily debit card withdrawal limits for certain cards to Rs 50,000-75,000.

- Bandhan Bank allows 3 free transactions in metro locations and 5 in non-metro locations; penalties apply beyond those limits.

- Failed transactions due to insufficient balance may attract a penalty fee.

What this means: Plan your ATM and UPI withdrawals more carefully to stay within free limits and avoid extra charges.

DIGITAL PAYMENTS Mandatory Two-Factor Authentication (2FA)

- The RBI now mandates two-factor authentication for all digital transactions, including UPI and card payments.

- At least one authentication factor must be dynamic - such as an OTP or biometric (fingerprint/face ID).

- Banks and fintech platforms may implement device binding or tokenization for additional security.

What this means: Expect an extra verification step (OTP or biometric) for every digital payment. A minor inconvenience that significantly reduces fraud risk.

PAN CARD PAN Application Rules Tightened

- Aadhaar alone is no longer accepted as proof of Date of Birth for new PAN card applications.

- Applicants must now submit additional documents such as a Class 10 certificate, passport, or voter ID.

- Existing PAN cards and those already issued are unaffected, this applies to new applications only.

What this means: If you are applying for a new PAN, ensure you have your Class 10 marksheet or passport ready before initiating the application.

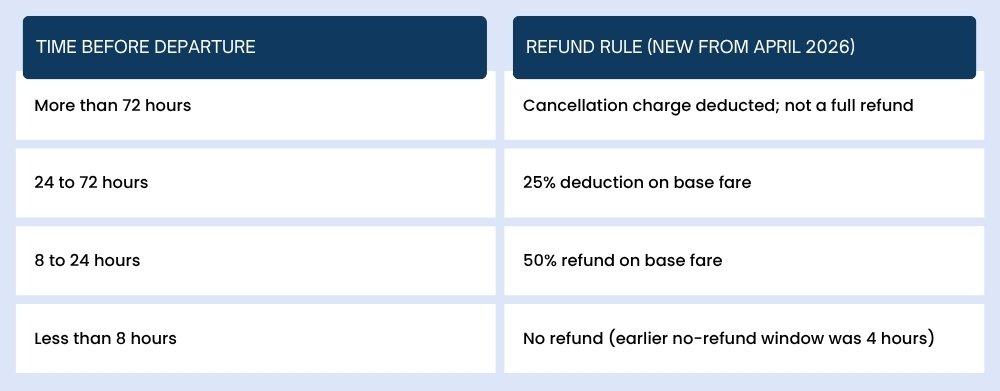

INDIAN RAILWAYS Revised Ticket Cancellation Policy

What this means: The no-refund window has doubled from 4 hours to 8 hours before departure. If you are prone to last-minute cancellations, plan and book accordingly.

FUEL PRICES LPG, CNG, PNG & ATF Revision

- Oil Marketing Companies (OMCs) revise fuel prices on the 1st of every month. April 2026 prices are being revised amid ongoing geopolitical pressures and supply disruptions in the Middle East.

- Domestic LPG cylinder prices (14.2 kg) may increase due to higher crude import costs.

- Commercial LPG, CNG, PNG (piped gas), and Aviation Turbine Fuel (ATF) are also under review.

- The Rs 300 subsidy for Ujjwala Yojana beneficiaries has been extended through FY 2026-27.

What this means: Household cooking costs and airfares may go up. Ujjwala Yojana households are partially shielded through the extended subsidy.

LABOUR LAW Salary Structure - Basic Pay Mandate

- Under the new Code on Wages, basic salary plus Dearness Allowance (DA) must constitute at least 50% of total CTC.

- As a result, both the employee's and employer's Provident Fund (PF) contributions will increase.

- Gratuity payouts will be higher as they are calculated on basic salary.

- Monthly take-home salary may reduce slightly in the short term, but long-term retirement benefits grow substantially.

What this means for HR teams: Payroll structures across all organizations need to be reviewed and reconfigured immediately. Payroll software should be updated to reflect the new basic pay calculation rules.

At a Glance: All Non-Tax Changes from April 1, 2026

Taken together, the regulatory changes on April 1, 2026, represent one of the most wide-ranging sets India has seen in a single financial year, spanning tax law, banking, travel, fuel, identity, and employment. Staying informed and acting early is the best way to minimize disruption and maximize benefits.

Staying Compliant Has Never Been More Critical; HR HUB Can Help

With 15 simultaneous changes to India's income tax framework, spanning payroll perks, TDS rules, ITR forms, and compliance deadlines, annual HR and payroll processes face a significant risk of errors and non-compliance. This is precisely where technology becomes essential.

HR HUB is a cloud-based HR and Payroll Management System trusted by businesses worldwide. It is built to adapt automatically to regulatory changes, so your team doesn't have to chase every amendment manually.

Whether you're managing 10 employees or 10,000, HR HUB ensures your payroll engine stays up to date with every regulatory change, giving your HR and finance teams confidence and time back.

Request a free demo at www.hrhub.app and see how HR HUB keeps your payroll compliant in FY 2026-27.